Homeowner’s Insurance in Colorado: What Buyers Need to Know Before They Close

shop homeowners insurance David Richins February 2, 2026

shop homeowners insurance David Richins February 2, 2026

Buying a home is one of the most meaningful financial decisions you’ll ever make. In Colorado—especially across the South Metro Denver corridor, Douglas County, and communities like Castle Rock, Parker, and Highlands Ranch—homeowner’s insurance isn’t optional protection; it’s foundational.

Think of it as the quiet safety net behind your mortgage. When it’s structured correctly, it protects your home, your belongings, and your financial future. When it’s misunderstood or under-estimated, it can become an expensive surprise.

Let’s break this down clearly, locally, and practically.

At its core, a homeowner’s insurance policy is designed to protect you in three major ways:

If your home is damaged by fire, hail, wind, or other covered events, your policy helps pay for repairs—or a full rebuild if necessary. This matters a lot in Colorado, where hailstorms, wind events, and wildfire risk can dramatically impact replacement costs.

Your furniture, electronics, clothing, and valuables are typically covered if they’re stolen or damaged. Many buyers underestimate how much it would cost to replace everything inside their home—until they have to.

If someone is injured on your property, your policy can help cover medical bills and legal costs. This is especially important for homes with pools, dogs, stairs, or frequent guests.

Financial authorities like NerdWallet consistently point out that homeowner’s insurance isn’t about probability—it’s about exposure. One major event without coverage can erase years of equity.

Over the last several years, homeowner’s insurance premiums have climbed nationwide—but Colorado has been hit harder than most states.

According to the Insurance Research Council, three factors are driving increases:

More frequent severe weather (hail, wind, wildfire)

Higher rebuilding costs (labor, materials, permitting)

Larger insurance claims across the country

When insurers pay more to rebuild homes, premiums rise to offset that risk. That’s the simple math behind it.

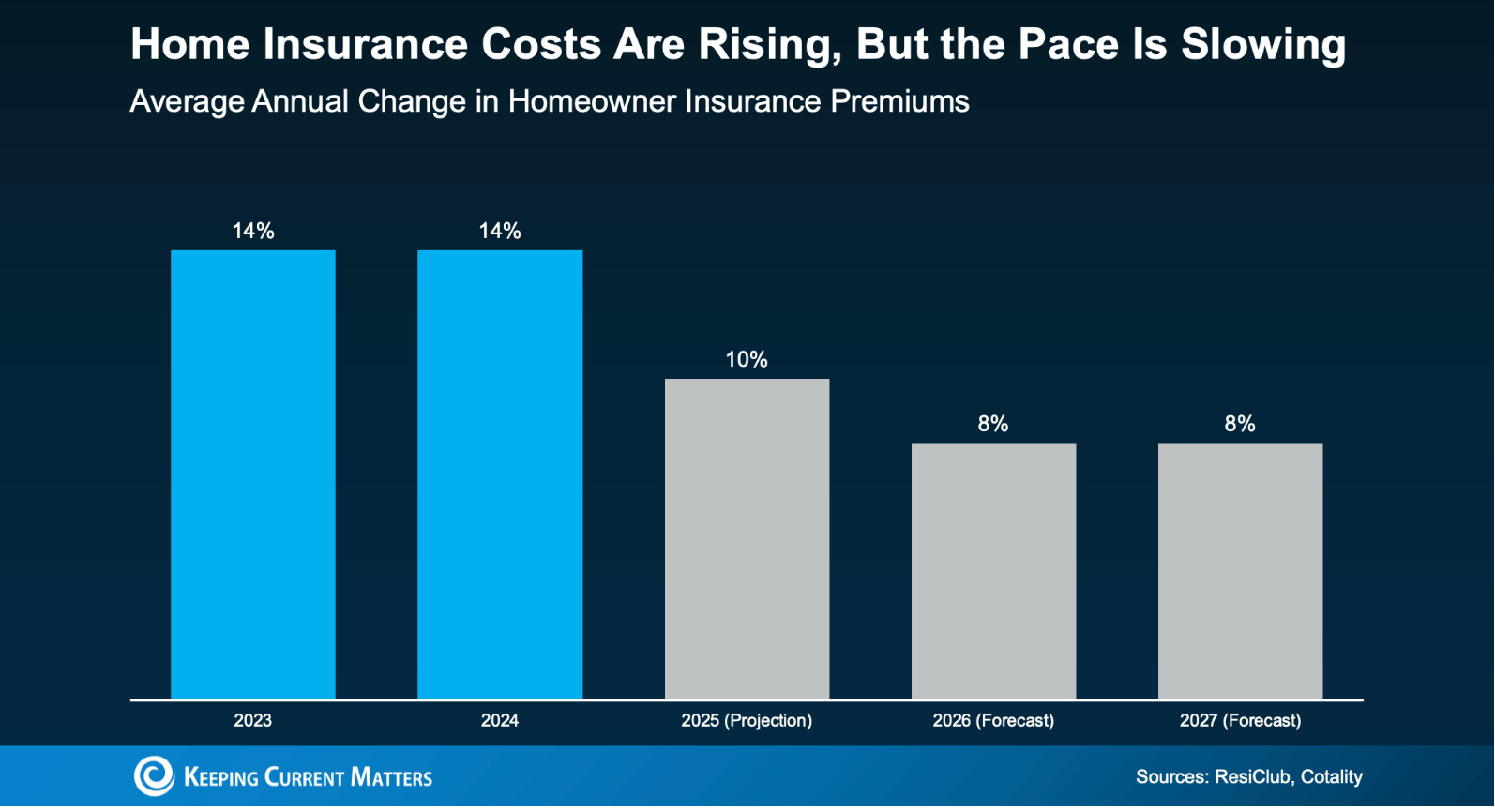

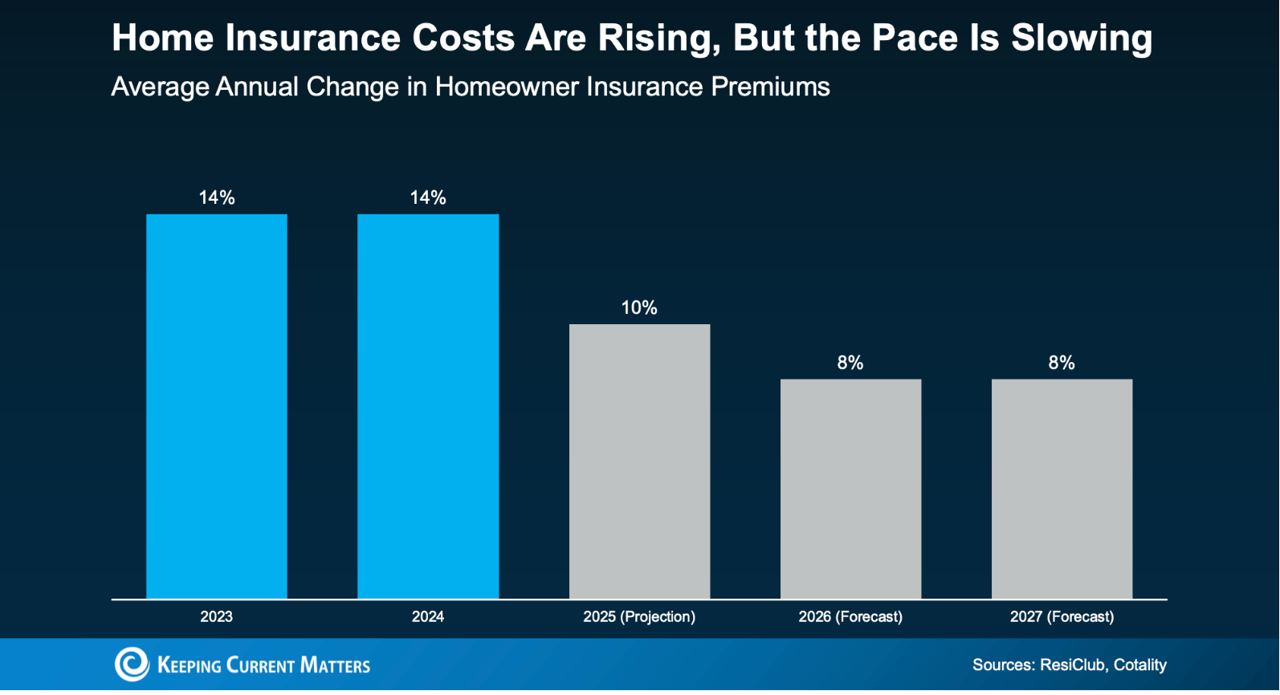

Industry data referenced by ResiClub and Cotality shows the pace of increases may finally be slowing:

2023–2024: ~14% annual increases

2025: ~10%

2026–2027 (projected): ~8%

That’s still an increase—but it’s no longer accelerating at the same pace.

Here’s where smart planning comes in.

While insurance premiums have risen, mortgage rates have eased, and that often offsets insurance and tax increases more than buyers realize.

As Michael Gaines, Senior VP of Capital Markets at Cardinal Financial, explains:

“Rising taxes and insurance do create pressure, but they don’t erase the benefits of a lower rate. A small rate improvement, paired with the right loan program and smart planning, can still make homeownership possible.”

The key takeaway: Home affordability isn’t determined by one factor—it’s layered.

Insurance premiums vary widely based on:

Location & ZIP code

Home value and rebuild cost

Roof type and age

Proximity to wildfire zones

Claims history in the neighborhood

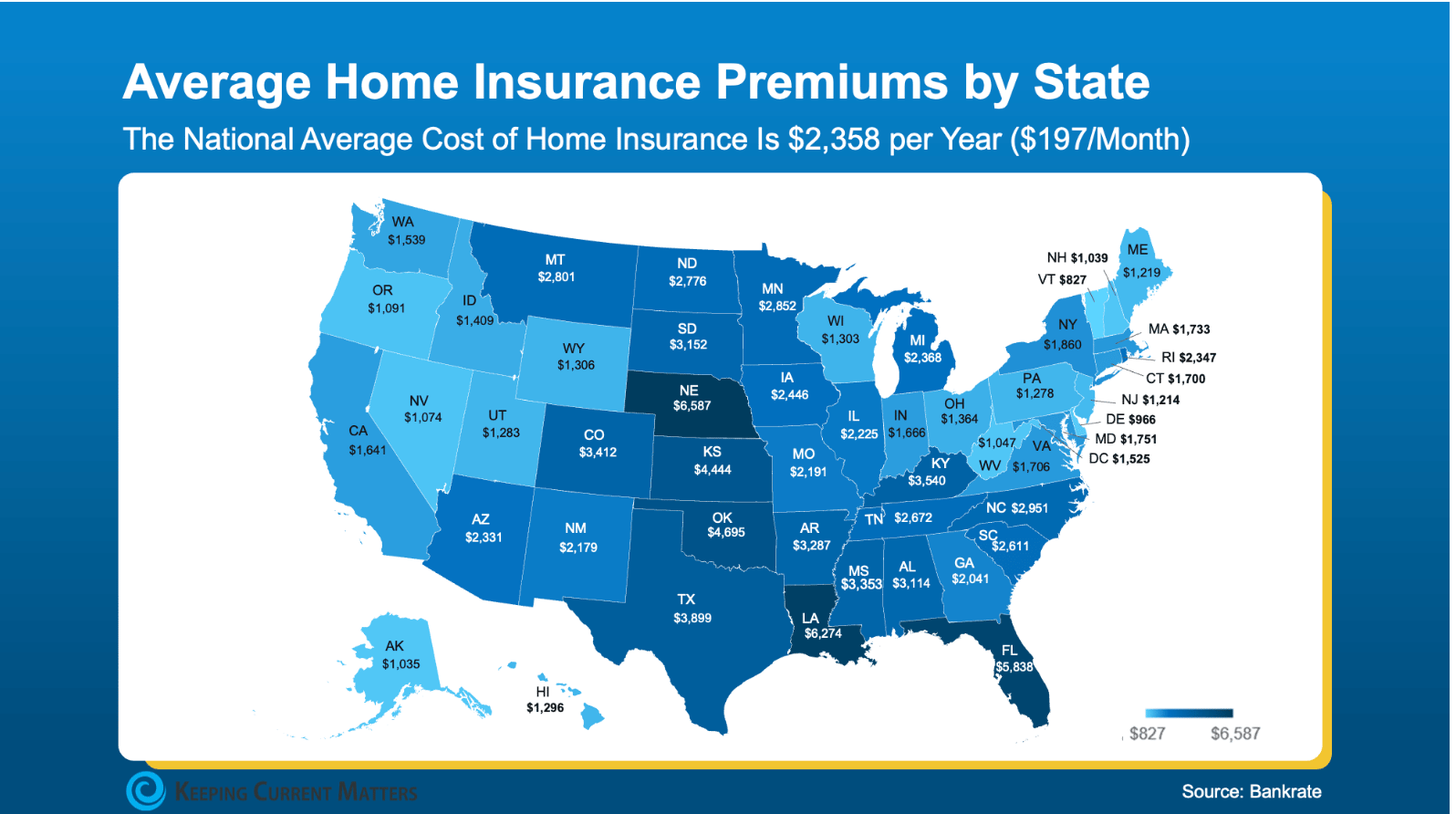

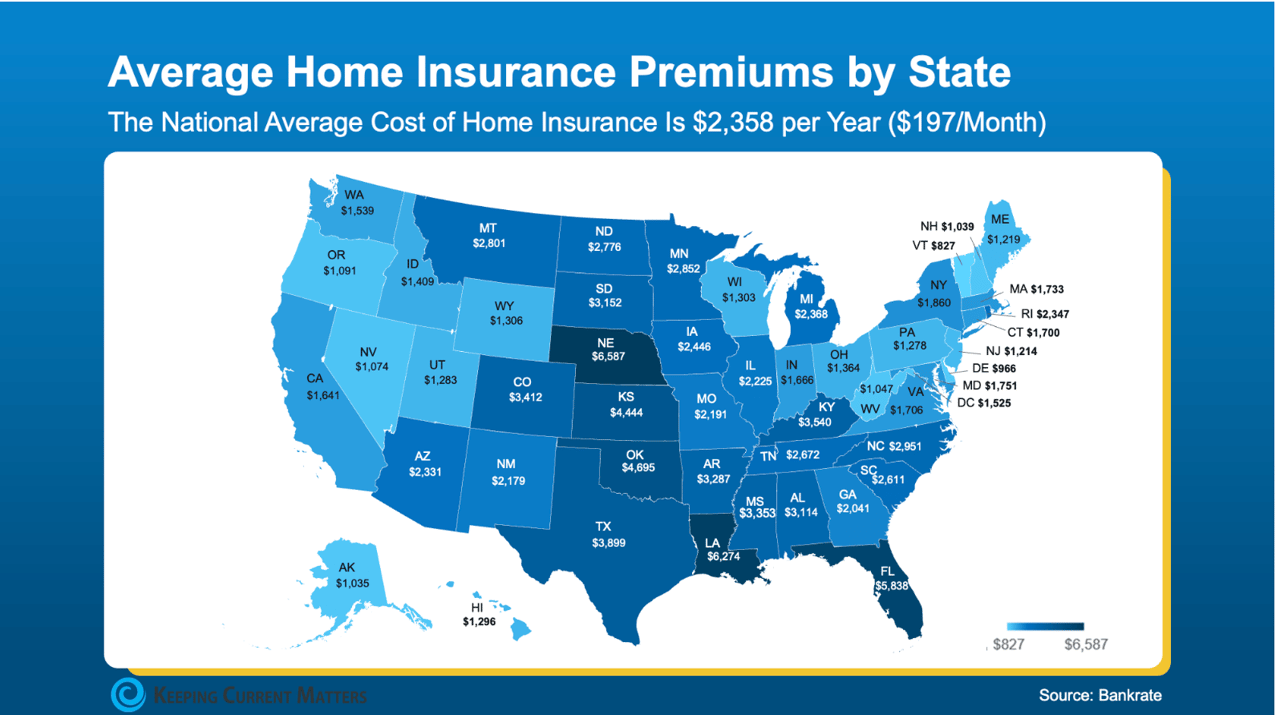

Two homes just miles apart in Douglas County can carry very different insurance costs.

That’s why online national averages don’t tell the full story—and why local guidance matters.

👉 If you’re searching homes in Castle Rock, Parker, Highlands Ranch, Castle Pines, Lone Tree, or Franktown, this should be part of your early budgeting conversation. Search Denver Homes for Sale

Your first year’s insurance premium is typically included in your closing costs. After that, it becomes a recurring expense—often escrowed into your monthly payment.

Here’s how experienced buyers keep it in check (sourced from NerdWallet and Insurify):

Shop multiple carriers – Rates vary more than most people expect

Bundle home & auto – One of the largest available discounts

Ask about discounts – New roofs, security systems, and impact-resistant materials matter

Highlight upgrades – Roof age, windows, and exterior improvements reduce risk

Protect your credit score – Credit still impacts premiums in many states

Pro tip: Always quote insurance early—before you fall in love with the house.

Homeowner’s insurance isn’t a line item to gloss over—it’s a strategic part of buying smart.

Yes, premiums have risen. But when you:

Understand local risks

Plan early

Shop intelligently

Pair insurance with the right mortgage strategy

…you put yourself in a far stronger position.

I help buyers across the South Metro Denver area layer smart financing, realistic insurance planning, and hyper-local market knowledge so there are no surprises at the closing table.

👉 Explore homes and resources at GoColoradoRealEstate.com

👉 Watch weekly market breakdowns on YouTube: Go Colorado Real Estate

👉 Reach out directly if you want a local, numbers-first strategy before you buy

Because protecting your home starts before you own it—and the best decisions are made with clarity, not headlines.

Stay up to date on the latest real estate trends.

Trust him for ultra-experienced, high-value real estate service in Englewood and South Metro Denver. With his 30+ years of market leadership, strategic insight, and personal dedication, he makes your buying or selling journey seamless and successful.